- Jakob Brezigar

- Updated: August 11, 2025

- Reading time: 6 min

How Trump's Executive Order Could Revolutionize 401(k) Plans with Crypto and Private Equity Access

President Donald Trump’s August 7, 2025 executive order could reshape U.S. retirement savings by allowing 401k plans to include crypto, private equity, and other alternatives.

The move aims to reduce regulatory barriers, offering new opportunities—and risks—for millions of American workers planning their financial futures.

Orcabay, an experienced market maker active on over 50 CEXs and DEXs — including Binance, Bitstamp, Kraken Coinbase, Uniswap — specializes in delivering tailored liquidity solutions. Contact us to learn more!

On Thursday, August 7, 2025, President Donald Trump signed an executive order that could make it easier for 401k and other workplace retirement plans to offer employees the option of investing some of their savings in alternative assets—including private equity, long the domain of institutional and “accredited” high-net-worth investors. The order seeks to “relieve the regulatory burdens and litigation risk” so employers that sponsor retirement plans can “apply their best judgment in offering investment opportunities to relevant plan participants.”

The immediate effect is not that every plan suddenly lists crypto or private funds on Monday morning. Rather, the order directs federal agencies—particularly the Department of Labor (DOL), and in coordination with the SEC and Treasury—to revisit guidance and rules that have historically made alternatives rare in 401k menus. That means a process of rulemaking and clarification before options reach many workers.

What is a 401k?

A 401k is a tax-advantaged retirement savings plan offered by many U.S. employers, allowing employees to contribute a portion of their salary into an investment account on a pre-tax or post-tax (Roth) basis. Employers often match a portion of these contributions, boosting employees’ savings. The funds grow tax-deferred until withdrawal, typically after age 59½, with early withdrawals subject to penalties.

The 401k was created through the Revenue Act of 1978, which added section 401(k) to the Internal Revenue Code. Initially intended as a tax provision for executives to defer bonuses, it quickly evolved into a mainstream retirement tool after the IRS clarified in 1981 that regular workers could also make salary-deferral contributions. Over time, 401ks largely replaced traditional pensions in the private sector, shifting retirement planning responsibility from employers to employees.

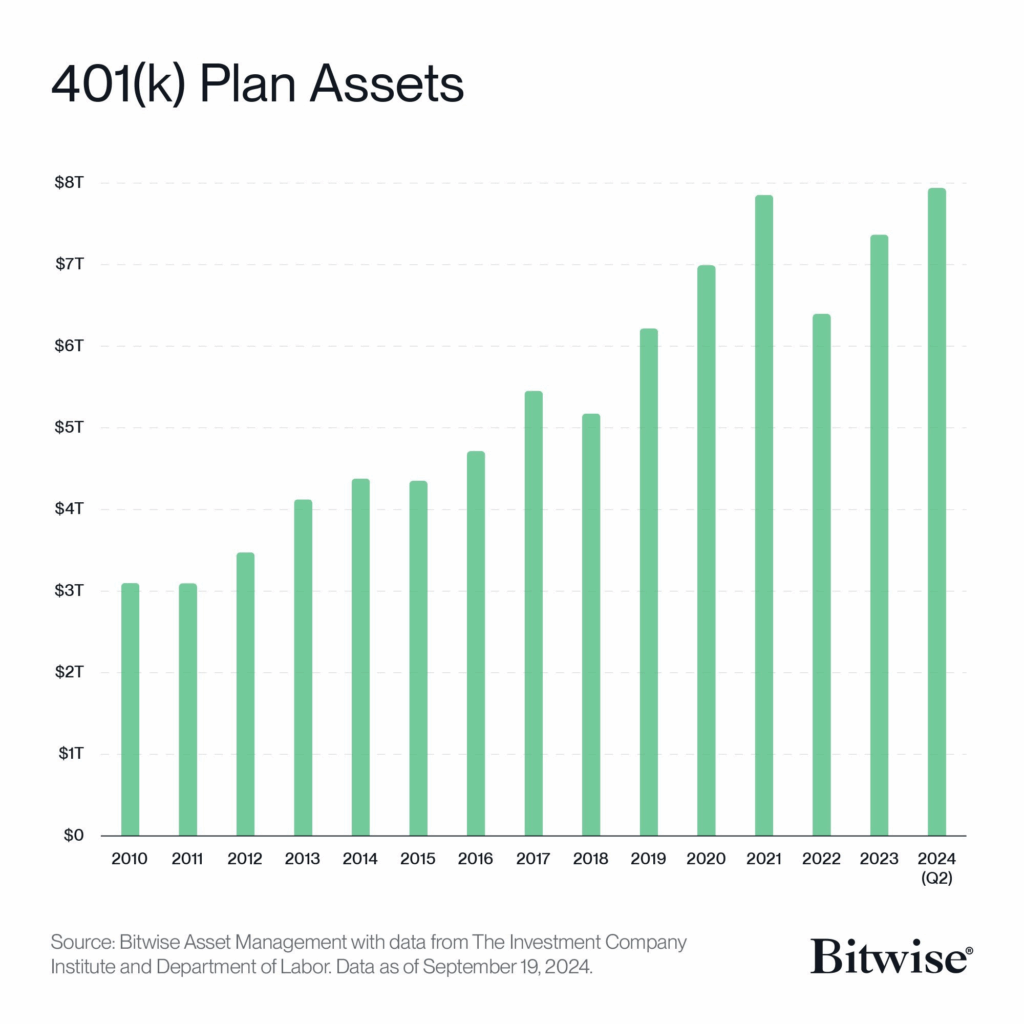

As of Q1 2025, approximately $8.7 trillion is held in U.S. 401k plans, across more than 715,000 plans and involving around 70 million active and retired participants.

What changes under the executive order?

AP News reports the order opens the door for higher-risk private equity and cryptocurrency investments to appear in 401k lineups—potentially granting those industries access to a pool of funds worth trillions. Still, the practical rollout depends on agency rule updates and plan-sponsor decisions, and could take time.

According to a White House fact sheet, the order instructs the Labor Department to re-examine fiduciary guidance for alternative assets in ERISA-governed plans, clarifies the appropriate fiduciary process for offering asset-allocation funds that hold alternatives, and directs coordination with the SEC and Treasury to align regulations. In short: fewer perceived legal obstacles for plan sponsors that want to evaluate alternatives—though fiduciary duties remain.

Impact on crypto

Once implemented, the order will grant Americans access to digital assets through their 401k plans, part of a multi-trillion-dollar retirement market and a sought-after opportunity for crypto firms aiming to reach more retail investors. The move would be a significant step forward for the crypto industry, which has long sought broader retail exposure and financial-system legitimacy. Despite institutional investors increasing crypto allocations, everyday savers have been restricted due to fiduciary risk, regulatory uncertainty, and volatility concerns.

Now, the executive order will not merely remove roadblocks but actively open the gates. According to Bloomberg data cited by Rasmussen, the U.S. 401k market is valued at approximately $12.5 trillion. (So, in simpler terms, the amount of money “locked” in U.S. 401k accounts ranges between $8.7 to $8.9 trillion, with the most recent figure being $8.7 trillion as of Q1 2025).

“In the US, roughly 100 million Americans have a retirement investment vehicle known as a 401k… Every 2 weeks, a portion of their paychecks are routed directly into purchasing a mixture of stocks and bonds… This is a HUGE driver of the equity market run and resilience over the past 20 years. A constant background bid for assets.” With around $50 billion entering these funds biweekly, even a modest portfolio allocation to crypto—1%, 3%, or 5%—could create recurring inflows of $120 billion to $600 billion annually. And these aren’t one-time flows. THEY KEEP BUYING ONCE ALLOCATIONS ARE SET,”

Tom Dunleavy, Head of Venture at Varys Capital.

Private equity, real estate, and other alternatives

While crypto is capturing headlines, the order’s scope extends to private equity and potentially real estate and other alternatives. Supporters say such exposure could diversify portfolios and potentially enhance long-term returns for some savers.

But these assets have characteristics—illiquidity, complexity, and fee structures—that differ substantially from typical index funds and bond funds in most retirement menus. AP News and ABC News both emphasize that opening access does not eliminate risk; it simply makes the options possible for plan sponsors who deem them appropriate and can meet fiduciary standards.

What happens next (regulatory path & timing)

Regulators must translate high-level direction into practical guardrails: due-diligence expectations, disclosures, default-fund considerations, and how alternatives could fit into target-date or managed-account frameworks.

The White House summary indicates inter-agency coordination, but each step—from proposal to final rule—takes time. As several outlets note, changes “would not be immediate”; most plans will move cautiously, if at all, until there is clarity on fiduciary processes and product design.

Potential issues and risks

While this move could give alternative asset managers access to a huge new pool of retirement money, some experts worry it might put Americans’ retirement savings at risk. Given all the due diligence fiduciaries will have to do, most workplace plan savers aren’t likely to be given a private-market option soon—and some may not see any changes at all. Analysts at PitchBook argued that “the executive order may remove some of the objections employers have had around incorporating private assets into 401k options, particularly concerns around litigation; however, it may not be enough to overcome cost concerns of employer 401k committees or resources to evaluate investments.”

Independent reporting underscores similar caution. Reuters points out that alternatives can bring higher fees, reduced liquidity, and transparency challenges, a stark contrast with the very low expense ratios typical in broad index funds that dominate 401k menus today. That trade-off—potential for higher returns versus higher risk and fees—will be central to how committees decide.

Who might benefit—and who should be careful

- Younger, risk-tolerant savers could view a small allocation to alternatives as a long-term diversifier, understanding volatility and the possibility of drawdowns.

- Near-retirees may decide the illiquidity/volatility trade-offs don’t fit their time horizon.

- Plan sponsors must weigh litigation risk, participant education, operational complexity, and cost against any expected portfolio benefits.

Across the board, investor education will be crucial. Even if alternatives appear on menus, they will likely arrive first inside professionally managed structures (e.g., multi-asset funds that cap alternative exposure), accompanied by robust disclosures and guidance.

Bottom line

President Trump’s August 7 executive order could reshape the 401k landscape by broadening the investment palette to include crypto, private equity, and other alternatives. For many savers, the decision won’t be whether to buy a private fund tomorrow, but how their employer’s plan evolves over the next several quarters as agencies finalize guidance and providers design products that meet fiduciary standards.

The opportunity is real—but so are the complexities and responsibilities that come with it.

Disclaimer: The information provided in this article is for informational purposes only and does not constitute financial, investment, or other professional advice. All opinions expressed herein are solely those of the author and do not represent the views or opinions of any entity with which the author may be associated. Investing in financial markets involves risk, including the potential loss of principal. Readers should perform their own research and consult with a licensed financial advisor before making any investment decisions. Past performance is not indicative of future results.

Jakob Brezigar

Jakob, an experienced specialist in the field of cryptocurrency market making, boasts an extensive international presence. With Orcabay, he has skillfully managed major operations and deals for a wide array of global stakeholders.