- Jakob Brezigar

- Updated: August 13, 2025

- Reading time: 6 min

Crypto Liquidity Providers vs. Crypto Market Makers – What Sets Them Apart?

In today’s evolving crypto markets, understanding the roles of crypto liquidity providers vs. crypto market makers is vital for token projects, exchanges, and institutional traders. While liquidity providers supply bulk capital—often via DeFi pools—to ensure trade execution and deeper order book depth, market makers actively engage in quoting bid‑ask spreads, dynamically managing inventory and price stability.

This expert overview by Orcabay distills key distinctions, performance metrics, real-world examples, and emerging regulatory and technological trends shaping the landscape through 2025 and into 2026.

Orcabay, an experienced market maker active on over 30 exchanges — including Binance, Bitstamp, and Coinbase — specializes in delivering tailored liquidity solutions. Contact us to learn more!

What is a crypto liquidity provider?

How do liquidity providers function?

A liquidity provider (LP) is typically an institutional or individual entity that provides large blocks of capital or tokens (e.g. ETH/USDT pairs on DeFi pools or prime broker quotations) to ensure trade execution and market depth on exchanges. LPs do not necessarily quote live bid‑ask spreads, but they support larger balloon trades and reduce slippage. In DeFi, LPs contribute equal value of tokens into a smart‑contract pool and earn fees proportionate to volume.

What metrics and KPIs do liquidity providers track?

- Total Value Locked (TVL): size of assets in a liquidity pool

- Utilization rate: ratio of utilized liquidity vs available capacity

- Fee revenue: basis points earned per swap

- Price impact/slippage metrics: measured per transaction size

- Withdrawal/storage risks and impermanent loss (in AMMs)

What is a crypto market maker?

How do market makers operate?

A crypto market maker (MM) is an entity that actively maintains two‑sided quotes (bid/ask), continuously updating prices and holding inventory. They profit from the bid‑ask spread and help stabilize prices, absorb volatility, and reduce slippage – often using algorithmic trading strategies and inventory models.

What KPIs matter for market makers?

- Average spread width and spread capture per trade

- Quote uptime (percentage of time two‑sided quotes are live)

- Matching flow: volume traded vs target

- Inventory turnover and hedging efficiency

- Rebate/incentive optimisation (e.g. via exchange maker‑taker programs)

Crypto liquidity providers vs. crypto market makers – What’s the difference?

What roles are distinct and where do they overlap?

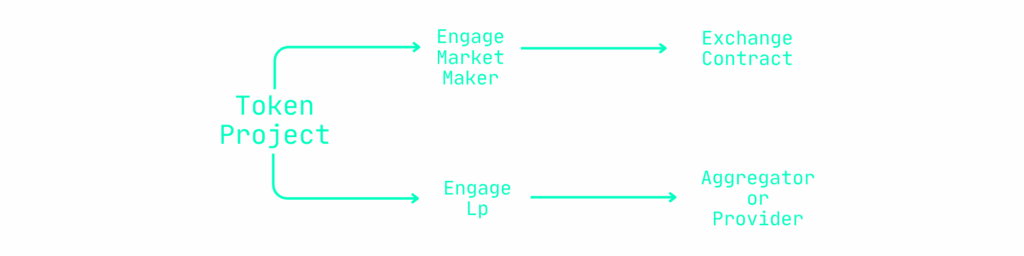

Market makers actively “make” the market by posting quotes and taking risk, while liquidity providers passively underwrite depth—they may not adjust prices live but supply capital to facilitate large trades. Ps often contract through aggregators; MMs may contract directly with exchanges to serve as designated market makers with quoting obligations.

| Feature | Liquidity Provider (LP) | Market Maker (MM) |

|---|---|---|

| Quote activity | Passive bulk liquidity | Active bid/ask quoting |

| Inventory risk | Lower; pooled capital | Higher; holds and manages asset inventory |

| Profit source | Fee on block trades or pool share | Spread revenue, rebates |

| Primary metrics | TVL, utilization, impermanent loss | Spread capture, uptime, inventory mgmt |

| Integration model | DeFi pools, prime brokers, aggregators | Exchange contracts, designated MM roles |

Real‑world and hypothetical examples

Example of a liquidity provider in DeFi

Suppose an LP deposits 100 ETH and 200 000 USDT into a Uniswap pool. They receive LP tokens, earn a share of swapping fees proportional to volume, and expose to impermanent loss if ETH/USDT price diverges. They do not actively quote prices but provide depth for zigzag trades.

Example of a centralized exchange market maker

An MM like Wintermute or Cumberland places continuous bids and asks on ETH/USD on a CEX. They maintain tight spread (e.g. 0.03%), adjust quotes algorithmically to manage inventory, and capitalize on spreads and exchange rebates. They guarantee uptime above 99% and maintain inventory within risk limits.

What regulatory and compliance frameworks apply in 2025–2026?

How does EU MiCA affect players?

Under MiCA (Markets in Crypto‑Assets Regulation), fully in force since December 2024, crypto‑asset service providers (CASPs)—including both LPs (in some cases) and MMs—must comply with authorization, capital requirements, governance, stress‑testing, and transparency obligations.

What about U.S. regulatory trends?

In 2025, U.S. regulators under SEC “Project Crypto” and the Trump administration’s roadmap have signaled major reforms: clearer classification of securities vs commodities, CFTC enforcement of spot markets for non‑security tokens, and creation of regulatory sandboxes.

Legislative proposals like the CLARITY Act and GENIUS Act aim to codify oversight, potentially classifying MMs supplying liquidity as regulated participants. Anticipated passage in 2025 or early 2026 may bring disclosure mandates, capital thresholds, and anti‑money‑laundering measures.

What trends should LPs and market makers watch into 2026?

Technological and market evolution

- AI‑driven algorithmic quoting will further sharpen inventory and risk management.

- Institutional adoption (e.g. banks exploring custody and trading under new U.S. clarity) is increasing.

- Hybrid models merging DeFi LP pools with active quoting—algorithmic “automated market makers” with active inventory hedging—will blur LP/MM boundaries.

Compliance evolution

- EU CASPs must meet MiCA governance and capital rules.

- U.S. legislation and regulatory frameworks expected by H1 2026 will require transparency around spreads, quoting practices, and AML/KYC at scale.

Conclusion: Key takeaways

- Crypto liquidity providers vs. crypto market makers play related but distinct roles: LPs provide capital depth (especially in DeFi), while MMs actively quote and stabilize prices.

- LPs measure success via TVL, utilization, fees, and slippage; MMs track spread capture, uptime, inventory controls, and rebates.

- Real‑world examples: LPs in AMMs like Uniswap; MMs such as Wintermute or Cumberland on centralized exchanges.

- Regulation is evolving: MiCA governs EU service providers, while U.S. frameworks like Project Crypto, CLARITY Act, and GENIUS Act will bring clearer oversight by 2026.

- Trends: growing institutional demand, AI‑enhanced quoting strategies, and hybrid liquidity models bridging DeFi and active market making.

- For token issuers, exchanges, or growth‑stage projects, understanding whether to engage LPs or MMs—or both—is crucial for liquidity resilience and regulatory compliance.

By integrating advanced liquidity engineering, regulatory readiness, and algorithmic insights, Orcabay offers strategic expertise in both LP and MM engagements—as trusted providers to token projects, exchanges, and institutional clients.

Disclaimer: The information provided in this article is for informational purposes only and does not constitute financial, investment, or other professional advice. All opinions expressed herein are solely those of the author and do not represent the views or opinions of any entity with which the author may be associated. Investing in financial markets involves risk, including the potential loss of principal. Readers should perform their own research and consult with a licensed financial advisor before making any investment decisions. Past performance is not indicative of future results.

Jakob Brezigar

Jakob, an experienced specialist in the field of cryptocurrency market making, boasts an extensive international presence. With Orcabay, he has skillfully managed major operations and deals for a wide array of global stakeholders.